From Woof to Poof:

Venture Capital

"In a world of scarce resources, globalization

without new technology is unsustainable."

― Peter Thiel

Pets.com is the best. Or more accurately, it’s one of the best examples of the complete insanity that was the dot.com bubble. Pets.com had a Super Bowl ad and a Macy’s Parade float but no real revenue. They lost $147m in the first nine months of 2000 but still managed to IPO (the stock originally traded up from $11 when it IPO’d in February of 2000 before the whole thing came crashing down a few weeks later, according to CNN). While just one of many examples, this seems to be what investors envision when they think of an overzealous venture market. The term I’ve heard frequently is “frothy.” Many investors believe that venture investing and specifically tech venture is once again becoming ‘frothy” and that we should be weary of some sort of repeat of Pets.com. The purpose of the below writing is to highlight all of the reasons why the landscape is very different now. Arguably, just about the only similarities are that all the companies both then and now have websites and that venture investing remains an optimist’s endeavor.

[CNN: http://money.cnn.com/galleries/2010/technology/%201003/gallery.dot_com_busts/index.html]

Let us first define the space and make some basic assumptions. For the sake of this writing, venture can be defined as early stage private equity capital in companies. In this case, we’ll narrow it even further to companies with a heavy technology component to their business model (fin tech, software, social media, e-commerce, et al) so we’re really talking about tech venture. As for assumptions, first let’s acknowledge that venture is an equity play and an illiquid one at that, so some stability at the broader economic level is important. If you believe that another 2008-like experience is around the corner, then none of the below will make a lot of difference. Second, let’s assume you can successfully (either directly or via a fund manager) execute a venture strategy. Among other things, this requires that you can: 1) identify and invest in good products and businesses, 2) invest at a decent valuation, 3) invest with others that are likely to improve the probability of success (more on this below). Clearly, this is easier said than done and there are innumerate books, articles, and fund managers who have ideas about how to do it best. What I have seen much less of is an objective look at venture in the context of where we are in the cycle today and what the landscape of today’s private markets looks like, so here it goes.

Landscape

Private markets have grown substantially in recent years, both in dollars and in the number of companies. In the late 90’s, investment banks big and small made tremendous amounts of money taking companies public. The information age offered the public unprecedented access to markets. Going public was all the rage. Got an idea and a website, we got capital for you! Since the bust, the trend has gone the other way. First, the bust created a distrust in the process, the bankers, and companies as a whole. If you want to go public now, you need to have every base covered, you need to be a slam dunk. Second, proliferation of private equity funds (venture included) created an additional level of private capital for companies, pushing the IPO further down the timeline. Third, volatility in public markets (even absent the major hiccups of 2000 and 2008) has made for truncated timeline expectations for investors. That quarterly or monthly performance focus is not necessarily congruent with the growth cycle of a mid-stage growth company. CEOs are not ignorant of that fact and subsequently weary about jumping into public markets. Last, increased regulatory scrutiny has added to the cost of doing business at the public level and incentivized many a potential IPO to wait it out a bit longer (see: Airbnb, Facebook).

On the other side of the equation, improvements in technology and communication have done wonders for entrepreneurs, especially since the 2008 crisis.

a) It is much cheaper now to start a business (tech) than it was in the late 90’s/early 2000’s. Improvements in information technologies have cut costs across the spectrum from marketing to accounting.

b) Online communication isn’t just cool, it’s necessary. There are something on the order of 50 times more internet users now with 180x the bandwidth and 6x the amount of time spent online, according to Both Sides of the Table. Facebook, Twitter, Linkedin allow for transmission of ideas and business initiatives faster than ever before.

[http://www.bothsidesofthetable.com/2014/06/29/why-venture-capital-is-so-much-more-compelling-now/]

c) It’s easier to get capital to start a business. While the traditional model of getting a loan from a bank is not what it used to be, necessity breads ingenuity and the cash strapped period around the 2008 crisis brought the world things like crowd funding, Angel List, etc. Additionally, stories like the guy who designed Facebook’s mural at their office, which they paid for with stock and now he’s a millionaire abound, peaking the interest of virtually every 30-something with a little expendable capital. Even convertible debt financing has alleviated the need for less active angel investors to get into the weeds (and legalese) of equity financing for early-stage tech companies.

Taken in total, private markets are growing in both depth and breadth. Fewer companies are IPO’ing later and the result is much deeper private markets. The breadth of the markets have also increased as cheaper start-up costs combine with greater access to capital. While none of this may translate into improving the chances of an individual start-up, it does mean there are a greater nominal number of opportunities for investors in private markets to capitalize.

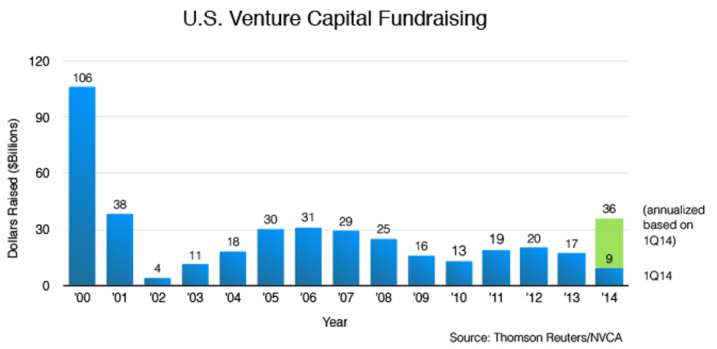

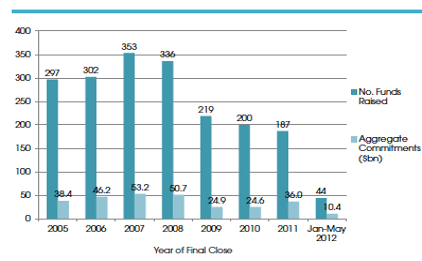

With the above as a backdrop, one might assume that the capital chasing these markets (and funds dedicated to such) are at all-time highs. That assumption would be inaccurate. Every chart there is shows a spike in the dot.com era in capital chasing venture that is orders of magnitude higher than before or after. The recent peak was 2006 and the below two graphs illustrate the landscape.

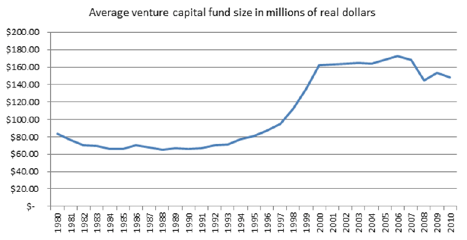

So, while funds and dollars are still in what one might call a normal range, the opportunity set is decidedly bigger. It’s worth noting that a frequent argument is that venture firms have just gotten bigger and bigger is bad in venture. The numbers however do not support all of that argument. On average, the change in the size of funds has been negligible. The firms that have gotten bigger have by and large done so on the back of good performance and success.

Source: NVCA

As a larger firm, there are a few factors that make the game a little different, but not all of them are bad. First, deploying more capital requires either later stage investments (which provide lower returns but should also translate to high probabilities of success) or investments in more projects (thus the influx in seed-staged funds and incubators such as Y Combinator). The challenge with the latter is that many of the liquidity events that happen for successful early-stage companies are not done at a level that would be enough to move the needle for a very large fund. Said differently, adhering to Peter Thiel’s maxim of investing in companies that could return your whole fund is even more difficult. On the bright side, venture investing has a large self-fulfilling component to it if you’re a large “name” fund. In other words, customers and future investors alike are more inclined to believe in and support a company because it has Sequoia or Andreessen Horowitz as an investor. This is also true because some of venture is hanging around long enough to figure out how to be successful and the support of deep pockets and seasoned advisors clearly makes that more likely. All in, while there is data to support a negative correlation between fund growth beyond a certain point and returns on average, it is fairly evident which firms are really average and which ones are still highly successful. It’s worth paying attention to the latter group. The little feeder fish that trails the successful great white does well too.

Navigating the Path

The path to venture success is simple in concept and difficult in practice.

1. Deal-Sourcing – There is a belief going around that the guys in Silicon Valley are just funding each other’s deals. Whether this is true or not, it is true that there is a lot of inside baseball in venture investing. There are two key steps to good deal sourcing:

a. Seeing the deal – leveraging the network of those that are connected to the best deals is imperative. Therefore, either piggy-backing off of or bringing a big name into a deal is a decent way to go. The other source is deep ties to the operators themselves, which can be achieved through dedicated staff (Andreessen model) or via the side door (like Bain Consulting and Bain Capital). [Note that Adam Bain has no relation to Bain Consulting or related entities.]

b. Winning the deal – the prettiest girl at the ball gets asked to dance a lot, why would she say yes to you? Again, this is where cultivating good relationships with the entrepreneurs can get you a long way. CEOs often want help and a little solicited advice, which is what has propelled YCombinator to wins with companies such as Airbnb and DropBox. They’ve built something from the ground up whereas heavy handed “advice” is not often appreciated.

2. Identifying the Path to Exit – with IPOs happening later, how will you monetize your success story? Again, it comes back to relationships, but in this case it is relationships with the prospective buyers. Roughly 95% of all venture-backed tech companies with successful exits are the result of an acquisition by one of about ten major companies. These are all household names at this point: Google, Yahoo, Cisco, Microsoft, Facebook et al. Many of these companies are cutting R&D budgets in favor of outside acquisitions (see: Facebook’s $19 billion acquisition of WhatsApp). It takes a lot of time to develop talent and projects in-house and there’s no guarantee the mousetrap you build is the best. In the fast moving technology space, many let the venture world be your R&D department and just pick the best stuff. This is happening across the major tech firms. Therefore, if you run a venture fund, it makes a lot of sense to develop very good relationships with the corporate development/acquisition people at these companies. If you knew what the Google team thought of Waze in 2010 when they raised $25m or 2011 when they raised $30m, you might have tried harder to get into those rounds. What’s amazing is how much the big tech firms will actually tell you about what they like and might acquire.

The venture world is maturing. Gone are the days of funding Pets.com with successful IPOs. Given the number of tech start-ups out there and the number of people who understand technology enough to be dangerous, the days of picking winners based purely on technological acumen are going away as well (too many options and less edge). Much like the hedge fund world is now pretty much devoid of “two guys in a room with a Bloomberg,” the venture world is likely to lose “two kids from Stanford who know how to code” venture funds. The successful venture firms are run by adults, guys who wear suits, and have spent years building the relationships described above and now required to navigate the path to exit. Those firms exist now and rather than being “frothy,” the venture cycle is in the early innings. Eventually, the cycle will repeat or at least rhyme. You’ll begin to see IPOs happen earlier again as Gen Y and the Millennials amass escalating amounts of disposable income and demand exposure. When the risk gets transferred to the public sector and retail is the end buyer, it might be time to get worried, but how long until that happens? Companies are now going from inception to $1bn in revenue in less than five years (Zulily, Ali Baba, etc.) so the venture cycle is accelerating and growth in the US more broadly is on a measured, but steadily upward slope. There’s money to be made in the new venture landscape and lots of it. As Sheryl Sandberg said at the 2012 HBS Graduation...

“Find a rocket ship and get on it.”